For decades, the financial world has been separated into two distinct, unequal camps. In one, you have liquid assets: public stocks, bonds, and cash that can be traded instantly, 24/7, from a phone. In the other, you have the “real” world: a multi-trillion-dollar universe of illiquid assets like real estate, fine art, private credit, and infrastructure. These assets are notoriously difficult to buy, sell, or manage, often trapped by paperwork, middlemen, and 9-to-5 market hours.

A new financial revolution is underway, and it’s not about creating new internet money. It’s about dragging the old money—all of it—into the digital age. This is the rise of Real-World Assets (RWA), a movement that uses blockchain technology to “tokenize” everything of value.

The premise is simple: What if you could buy and sell a 1% stake in a Manhattan apartment building as easily as you buy a share of Apple? What if a small business could secure a loan by using its warehouse inventory as real-time, on-chain collateral?

This isn’t a distant fantasy. It’s a market that financial giants like BlackRock, JPMorgan, and Citi, along with the Boston Consulting Group, predict could swell to over $16 trillion by 2030. This is the story of how blockchain is moving from a niche curiosity to the foundational plumbing of the next financial system.

The Trillion-Dollar Problem: Why “Real” Assets Are Broken

The most valuable assets in the world are fundamentally inefficient. The current system is plagued by three core problems that blockchain technology is uniquely poised to solve.

- Illiquidity: If you own a $1 million commercial property, you can’t easily sell 5% of it to pay for an expense. You’re all in or all out. Selling it requires brokers, lawyers, and months of paperwork, locking up your capital.

- Fractionalization Barriers: This illiquidity makes high-value assets inaccessible. Want to invest in a “blue-chip” Picasso painting? You’ll need tens of millions. Want a stake in a high-performing private equity fund? You’ll need to be an accredited investor with millions to commit for 5-10 years.

- Inefficient Operations: Traditional finance runs on a complex, trust-based web of intermediaries. Settling a simple stock trade still takes two days (T+2). Cross-border payments are slow and expensive. Every step involves a different ledger, a different middleman, and a different fee.

The “Tokenization” Solution: How It Actually Works

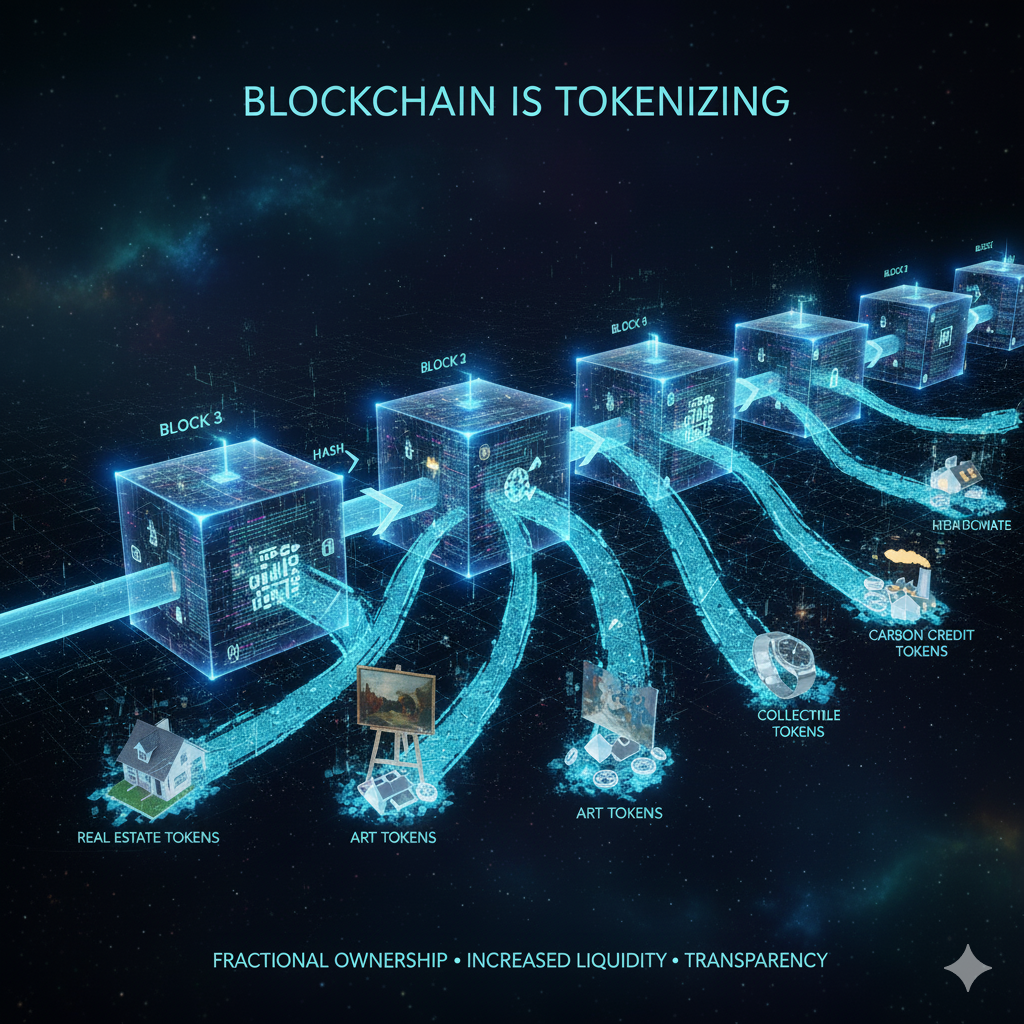

Tokenization is the process of creating a digital token on a blockchain that represents ownership of a real-world asset. This digital token acts as a “digital twin” for the asset, inheriting its value and legal rights.

This process isn’t magic; it’s a sophisticated stack of three key technologies:

- The Blockchain (The Digital Ledger): This is the database where ownership is recorded. Instead of a deed in a dusty filing cabinet, you have a token in a digital wallet. Institutions are flocking to chains like Ethereum for its security, Polygon for its low fees, and Avalanche for its “Subnets,” which let them build private, compliant-ready blockchains.

- The Smart Contract (The Automated Engine): This is the code that defines the asset’s rules. A smart contract can be programmed to automatically:

- Distribute rental income from a tokenized building to all token holders on the 1st of each month.

- Pay out a bond’s coupon.

- Block a transfer to any wallet that hasn’t completed KYC (Know Your Customer) checks. This automates the work of administrators, accountants, and transfer agents, slashing costs and errors.

- The Oracle (The Data Bridge): A blockchain can’t see the outside world. It doesn’t know the interest rate, the market value of a building, or if a shipment arrived. Oracles, like the industry-leading Chainlink, are secure services that feed this vital off-chain data to the smart contract. This is the magic link that allows a smart contract to react to real-world events.

The Revolution in Practice: From Theory to BlackRock

This ecosystem is already live and handling billions of dollars.

- Bonds and Treasuries: This is the RWA “killer app.” The $100 trillion global bond market is notoriously archaic. Today, financial giant BlackRock has a tokenized fund, BUIDL, on the Ethereum blockchain. It allows investors to buy a token that represents a share in a U.S. Treasury money market fund. This token can be transferred 24/7, used as collateral in decentralized finance (DeFi) protocols, and settles instantly—a massive upgrade over traditional finance.

- Real Estate: Platforms like RealT are “fractionalizing” residential properties. You can go on their site and buy a $50 token representing a sliver of a home in Detroit. The smart contract then automatically collects rent and deposits it into your crypto wallet as stablecoins—you are quite literally “cashing rent” every day.

- Fine Art & Collectibles: Do you want to own a piece of a Warhol or a Basquiat? Platforms like Masterworks have built a billion-dollar business by doing just that. They buy a blue-chip painting, file it with the SEC, and then “tokenize” it, allowing anyone to invest in shares of the artwork, hoping it appreciates in value.

The Hurdles: Why Hasn’t This Taken Over?

If this technology is so revolutionary, why isn’t everything tokenized already? The answer lies in three significant challenges.

- The Regulatory Sledgehammer: In the U.S., the primary question is: “Is this token a security?” Under the 1946 Howey Test, most tokenized assets (which represent an investment in a common enterprise with the expectation of profit from the efforts of others) are clearly securities. This subjects them to a massive body of law, which the crypto world has often tried to ignore. In contrast, the European Union has provided a clearer path with its MiCA (Markets in Crypto-Assets) and DLT Pilot Regime, fostering more structured innovation.

- The Oracle & Security Problem: The system is only as strong as its weakest link. If the oracle feeding the price of a building is wrong or manipulated, the entire system breaks. A bug in the smart contract code could lead to a catastrophic loss of funds. This makes institutional-grade security audits and robust, decentralized oracles an absolute necessity.

- Valuation and Liquidity: Tokenizing a building doesn’t magically make it liquid. You still need a buyer. The “valuation problem” isn’t solved by the blockchain; you still need a real-world appraisal to determine the asset’s worth. While a 24/7 market is possible, it doesn’t guarantee a deep pool of buyers and sellers.

The Future: A $16 Trillion Convergence

The barriers are high, but the momentum is undeniable. The future is not about “crypto” replacing “traditional finance.” It’s about a “great convergence” where the efficiency, transparency, and speed of blockchain technology are used to upgrade the rails of the entire financial system.

The benefits are too large to ignore: a 24/7 global market, the disintermediation of costly middlemen, and the “unlocking” of trillions in illiquid assets. This new, tokenized infrastructure will allow for a wave of financial products we can’t even imagine—portfolios that automatically manage real estate, bonds, and art, all represented by tokens in a single wallet, all working for you, 24/7.